Pullbacks are the stubbed toe of the stock market. Our LPL Research analyst shared that he was reminded of this over the last week as he contemplated the recent surge in volatility while picking up toys after his two-year-old finally fell asleep. As he carried a Tonka truck back to its usual parking spot next to the toy farm, he slammed his toe into the foot of the couch. The pain was acute, but not worthy of a full-blown panic. After a few deep breaths, the sting began to wear off and he assessed the damage to find a little redness, but nothing broken. Somewhere in this painful process, the parallels between his toe’s unfortunate encounter with the couch and the recent equity market sell-off became clear. For the market over the last week, the foot of the couch was embodied by overbought conditions — especially in big tech, waning confidence for a soft landing due to weak employment data and a contractionary Institute of Supply Management (ISM) manufacturing reading, and the rapid unwinding of the crowded yen carry trade.

Pullbacks in the equity market are inevitable, something investors tend to forget during periods of low volatility. When they occur, they tend to be painful and spark fear over something breaking. The market narrative often shifts during these periods as waning optimism manifests into panic, an emotion evident on the CBOE Volatility Index (VIX) last week. The VIX or ‘fear gauge’ surged to its highest reading since March 2020 on August 5 (a rising VIX is associated with increased fear and uncertainty in the market, and vice versa for a falling VIX). We view this move — and its subsequent decline — as a constructive sign, as major spikes in the VIX often overlap near capitulation points in equity markets.

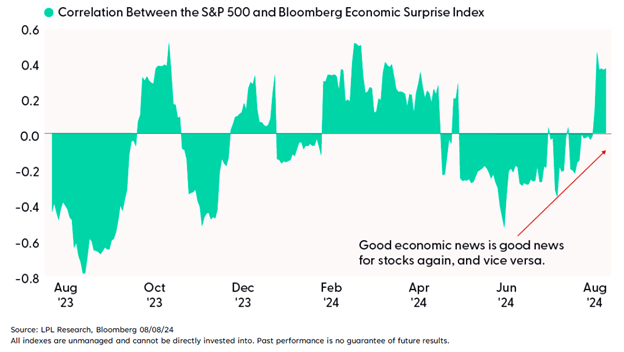

The change in the market narrative became especially pronounced over the last week. The chart below highlights the rolling one-month correlation between the S&P 500 and the Bloomberg U.S. Economic Surprise Index. (For context, the surprise component is based on the percentage difference between an actual economic data release and the median analysts’ forecast.) When the correlation is positive, it implies good economic news is good news for the broader market, and vice versa. When the correlation is negative, good economic news tends to be bad news for the broader market, and vice versa.

As you can imagine, it has been a busy couple of weeks for LPL Research as their team published an array of content related to the jump in equity market volatility. To boil down this work into one simple message for investors, don’t panic. While such sharp declines in equity prices are concerning, looking back at historic data on the S&P 500 index reminds us that dips, pullbacks, and even corrections of 10% or more are a normal and healthy part of any bull market. On average, stocks experience a pullback of over 5% over three times per year and a correction of 10% or more around once per year — even in positive years. Expressing this data another way, 94% of years since 1928 have experienced a pullback of at least 5%, and 64% of years have had at least one 10% correction. We believe that how common these occurrences are should provide comfort to equity investors, allowing them to be patient, stay invested, and most importantly, to not panic.

~Mark and Elise

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. All investing involves risk including loss of principal. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful. All information is believed to be from reliable sources; however, LPL makes no representation as to its completeness or accuracy. This research material has been prepared by LPL Financial LLC. Tracking #616374-1 (Exp. 8/25).

Retirement Planning

Retirement Planning Asset Management

Asset Management Education Planning

Education Planning